Latest figures show cattle prices rising, but a big fall for finished lambs

6th August 2021

The latest reporting figures from AHDB are showing a mixed picture across livestock, with cattle on the rise, pigs remaining stable, and sheep taking a decline.

Across all livestock, figures from AHDB do show a price increase compared to the same time last year, but there are still some disappointments to be felt by farmers – with cattle prices rising but a big fall for finished lambs.

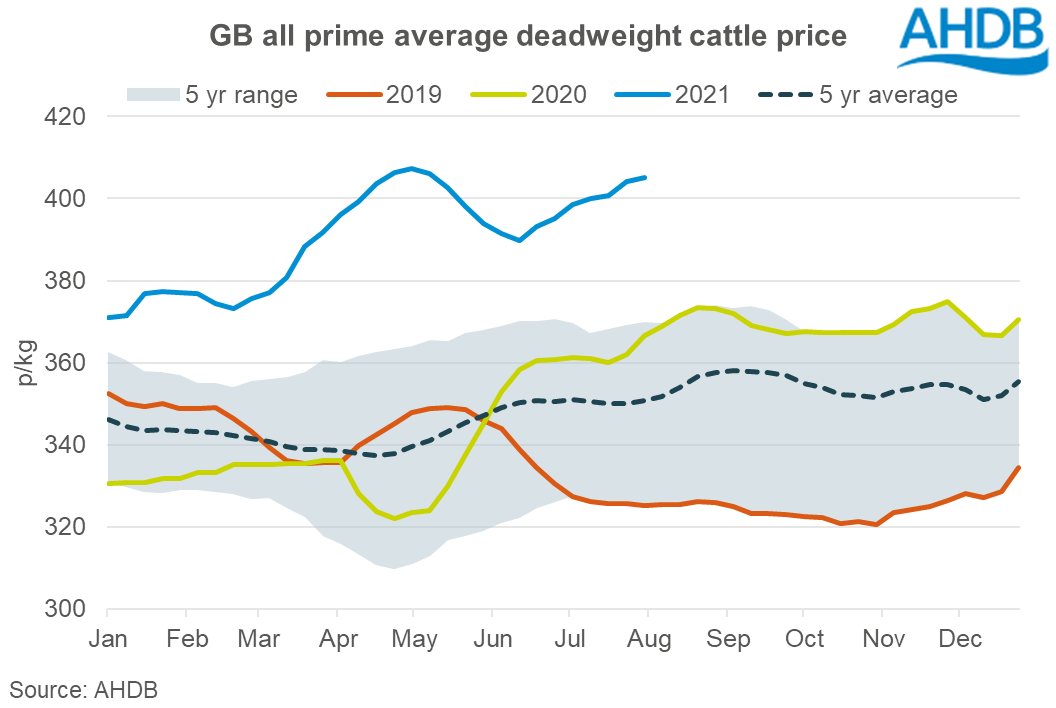

The best results are being seen by beef farmers, with prime cattle prices rising across the board in the latest reporting week.

In the week ending 31st July, the GB all-prime average deadweight cattle price rose by 1.0p to average 405.1p/kg. This is up 38.6p on the price for the same week a year ago.

Throughput of prime heifers, steers and young bulls at British abattoirs was estimated to be 32,100 head for the week. This was 6 per cent higher than the week before, but still down on the same week last year (-2%).

2021 slaughter so far is estimated at 989k head. This is slightly above the levels recorded in each of the years from 2016 to 2019, and is, therefore, also above the five-year average, by a modest 0.3 per cent.

GB deadweight prime cattle price movements (w/e 31 July):

All prime: 405.1p/kg up 1.0p

Steers (overall): 406.4p/kg up 1.2p

Steers (R4L): 415.1p/kg up 1.2p

Heifers (overall): 405.2p/kg up 1.2p

Young bulls (overall): 399.9p/kg up 0.8p

Overall cull cow prices fell back this week, down 1.4p to average 292.4p/kg. Prices have been at, or around, the 292p/kg mark for four weeks now. Cows of -O4L spec did show an increase, up 2.4p to 314.4p/kg. Cow kill at GB abattoirs was estimated to be 10,100 head during the week. While this is up 7 per cent on the week before, it is down -3 per cent on the same week last year. For the year-to-date, estimated cow slaughter stands at 301k head, down 5 per cent on the same period in 2020. Unlike prime slaughter, cow slaughter is also down on 2019 (-5%) and the 5 year average (-3%).

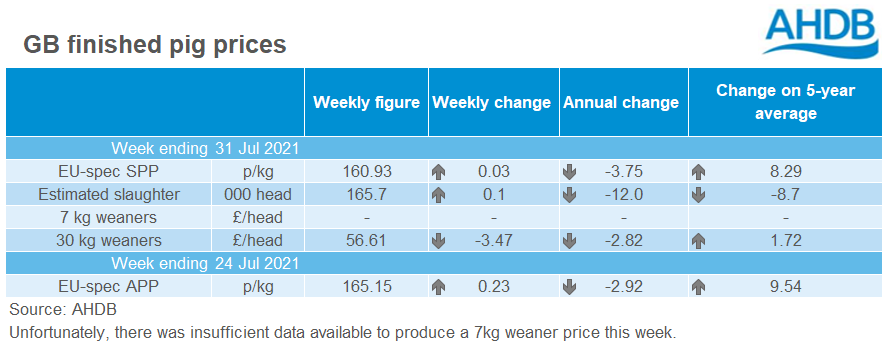

In the same reporting week, ending 31st July, the price of finished pigs also managed a small increase, continuing a steady upward trend. Prices are currently seeming quite stable with the GB EU-spec SPP averaged 160.93p/kg, a modest increase of 0.03p on the week before. The measure is now just 3.75p below the price achieved for the same week a year ago.

Carcase weights averaged 86.44kg for the week, down 170g on the week before, but 660g heavier compared to the same week a year ago.

Clean pig slaughter was estimated to be 165,700 head for the week, similar to the week before (+100 head). Throughput was well below last year’s level for the third consecutive week.

Unfortunately some concerns are starting to be raised as Covid-related staffing issues occur in some abattoirs. As slaughter totals remain well below what they were last year, staffing problems could escalate the problem and push numbers well down.

In the week ending 24th July, the GB EU-spec APP rose 0.23p on the week before to average 165.15p/kg.

Meanwhile, 30kg weaners averaged £56.61/head in the week ending 31st July, down £3.47 on the week before.

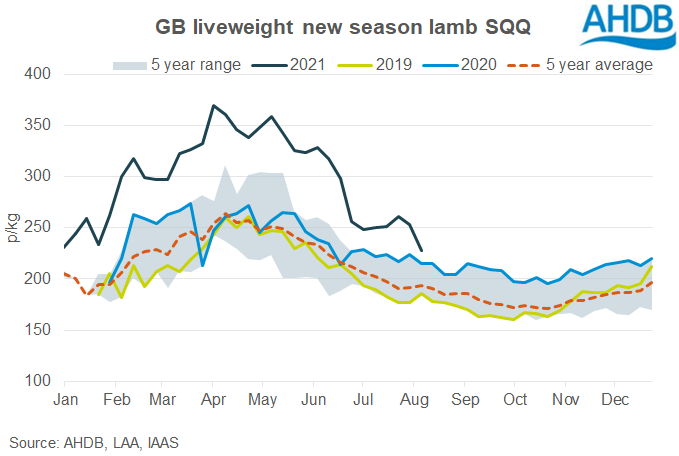

Meanwhile, the picture is unfortunately not so positive for sheep farmers, with liveweight lamb prices taking a dramatic dip. In the week ending 4th August the GB liveweight NSL SQQ fell 25p, to 227.46p/kg. Weekly throughputs were back 12 per cent, week-on-week to 102,000 head. The latest prices are higher than the same time last year, but are still likely to be a disappointment to farmers.

The drop in lowered price is thought to be a result if weakened export demand. With British and Irish finished lamb prices having been above their French counterparts for the past few weeks. Whenever this is the case farmers can expect a sudden decline in price as the export market looks to cheaper alternatives.

In contrast to recent falls in liveweight prices, the GB deadweight NSL SQQ gained 5p in the week ending 31st July to stand at 565.5p/kg. Estimated kill for the week was up 6 per cent on the week, to 220,000 head.